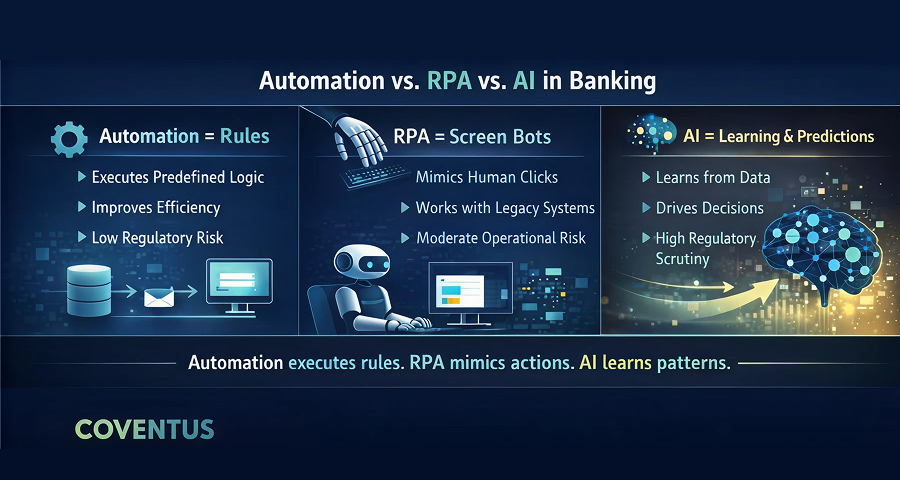

Automation executes rules, RPA mimics human actions, and AI learns patterns, and each carries a different regulatory and risk profile in banking.

The banking industry is in the middle of a massive transformation. Every institution, from community banks to global players, is looking for ways to streamline operations, reduce costs, and improve customer experience. That’s where automation, RPA, and AI come in.

But these terms get mixed up all the time. Vendors blur the lines. Internal teams use them interchangeably. And regulators? They care deeply about the differences.

If you’re a bank leader trying to modernize safely and strategically, understanding these distinctions isn’t optional; it’s foundational.

Let’s break it down clearly.

1. Automation: The Foundation

Automation is the broadest category. It refers to any technology that performs tasks without manual effort.

Think of it as the digital equivalent of “set it and forget it.”

Examples in banking

- Workflow routing (send this loan to underwriting)

- Automatic notifications to customers

- API-based data transfers between systems

- Batch jobs that run overnight

- Rules engines that check eligibility

Why banks use it

- Reduce manual work

- Improve consistency

- Eliminate human error

- Speed up processes

Risk profile

Low to moderate.

Automation is rules-based, deterministic, and easy to explain, which regulators like.

2. RPA: Automation That Mimics Human Actions

RPA (Robotic Process Automation) is a specific type of automation that uses software “bots” to mimic human actions on a screen.

If automation is the umbrella, RPA is one tool under it.

Examples in banking

- Bots logging into the core to download reports

- Bots copying data from Excel into the LOS

- Bots reconciling transactions across systems

- Bots pulling statements from vendor portals

Why banks use it

- Works well with legacy systems

- Fast to deploy

- Doesn’t require APIs

- Reduces repetitive manual tasks

Risk profile

Moderate.

RPA is powerful but fragile. If a screen changes, the bot breaks.

Banks must manage:

- Change control

- Exception handling

- Monitoring

- Audit trails

3. AI: Automation That Learns

AI (and machine learning) is where things get interesting and risky.

AI doesn’t follow rules.

It learns patterns from data and makes predictions or recommendations.

Examples in banking

- Fraud pattern detection

- AI-assisted underwriting

- Intelligent document classification

- Chatbots that generate responses

- Predictive customer insights

- Credit line management

Why banks use it

- Better accuracy

- Faster decisions

- Improved customer experience

- Ability to detect patterns humans miss

Risk profile

High.

AI introduces:

- Model risk

- Fair lending risk

- Bias and disparate impact

- Explainability challenges

- Data privacy concerns

- Drift and performance decay

This is why AI falls under OCC 2011‑12 and SR 11‑7. The same rules that govern credit models, AML models, and stress‑testing models.

4. How Banks Should Think About the Three

- Automation = Efficiency

- Use it to streamline processes and reduce manual work.

- RPA = Band-Aid for Legacy Systems

- Use it when APIs don’t exist, or systems can’t integrate.

- AI = Intelligence

- Use it to improve decisions — but only with strong governance.

| Dimension | Automation | RPA (Robotic Process Automation) | AI / Machine Learning |

|---|---|---|---|

|

What it is |

Any technology that performs tasks without manual effort |

A type of automation that mimics human clicks/typing in software |

Systems that learn patterns from data to predict, classify, or decide |

|

Logic type |

Rules-based |

Rules-based |

Pattern-based, probabilistic |

|

How it works |

Workflows, scripts, APIs, triggers |

Bots interact with screens like a human |

Models trained on data; adapt over time |

|

Examples |

Workflow routing, auto-approvals, API integrations |

Bot logging into LOS to copy data, downloading reports |

Fraud detection, underwriting support, chatbots, document intelligence |

|

Deterministic? |

Yes. Same input → same output |

Yes. Unless screen changes |

No. Outputs vary based on learned patterns |

|

Explainability |

High |

High |

Lower. Requires explainability tools |

|

Risk profile |

Operational risk |

Operational risk (breaks easily) |

Model risk, fair lending risk, privacy risk |

|

Regulatory lens |

IT controls, change management, auditability |

IT controls, operational risk |

OCC 2011-12, SR 11-7, ECOA/Reg B, UDAAP, privacy laws |

|

Data requirements |

Accurate input data |

Accurate input data |

Training, validation, monitoring, drift detection |

|

Human oversight |

Recommended |

Recommended |

Mandatory for regulated decisions |

|

Vendor expectations |

Security, reliability, continuity |

Same as automation |

All of automation + model documentation, validation support, fairness testing |

|

Where banks use it |

Operations, servicing, reporting, workflows |

Repetitive tasks, legacy system integration |

Credit, fraud, AML, marketing, customer service |

|

Failure mode |

Workflow breaks |

Bot breaks when UI changes |

Model drift, bias, false positives/negatives |

|

Board-level question |

“Is it controlled and auditable?” |

“Is it stable and monitored?” |

“Can we explain and defend these decisions to regulators?” |

5. Why the Differences Matter for Banks

Regulators don’t treat these technologies the same, and neither should your risk teams.

| Category | Automation | RPA | AI |

|---|---|---|---|

|

Logic |

Rules |

Rules |

Patterns |

|

Explainability |

High |

High |

Lower |

|

Regulatory scrutiny |

Low |

Moderate |

Very high |

|

Fair lending risk |

Low |

Low |

High |

|

Model risk |

Low |

Low |

High |

|

Operational fragility |

Low |

Moderate |

High (drift) |

|

Governance needed |

IT controls |

IT + Ops |

Full MRM lifecycle |

- Audit findings

- Model risk citations

- Fair lending exposure

- Operational failures

Banks need different controls for each category.

6. The Bottom Line

Automation, RPA, and AI are not interchangeable.

They solve different problems, carry different risks, and require different controls.

Banks that understand these differences can modernize confidently. Banks that do not do so risk regulatory trouble, operational failures, and customer harm.

The winners in the next decade of banking will be the institutions that adopt automation strategically, RPA carefully, and AI responsibly.

Modernize your banking operations with confidence. Coventus helps you deploy automation strategically and AI responsibly.

Reach out to start your modernization journey securely.